Over the past few years countries which have a forward looking approach to where the future is headed, in order to avoid their own ‘Kodak’ moment, have invested in securing critical minerals/metals needed to be part of that future.

There was a report put out in May of 2019 by FP Analytics called :

Which detailed, up until that time, China’s dominance in securing critical metal refining capacity as well as the raw material supply chain – ie. Vertical integration by owning the mine or mining company. This report looks at many of the materials on the RIO/MIT chart including Rare Earths, Graphite, Lithium, Vanadium, Cobalt, Vanadium, Gallium, Indium as well as Platinum group metals, Niobium amongst others.

It also appears the US, Canada, Australia, India, Europe all have had a similar focus in securing the same.

And classified them similar to the earlier version MIT produced based on type of technology served by that mineral.

As mentioned earlier, there is a general consensus that the next Decade will be one where battery factories are built across Europe with a myriad of auto-manufacturers committing to EVs in a very big way.

Also mentioned earlier was the large number of common sector investments the likes of Softbank (Japan), Bezos / Amazon (USA) & the international team from the Breakthrough Energy Ventures have backed as part of their decarbonization portfolio.

This type of spread investment risk in developing technologies is not limited to these three, but large industrial organisations such as Sumitomo (Japan) & even fossil fuel organisations like Koch Industries (USA) have similar approaches.

Although I’m not yet able to provide a comprehensive picture of whether Australia has assembled something similar (I can certainly see one being built) & haven’t looked to other major industrial companies from advanced economies (South Korea, China for instance), what does immediately come to mind is whether Europe has anything similar?

So now I have to tell you what got me started down this entire line of research & prompted me to put this thread & website together – it was a fairly innocuous post on an investment forum in Australia. This was the start of the thread.

The reason this particular list of companies raised my curiosity is that a couple of these companies & I am by no means a large investor, were companies which I’d put money into with the belief that at some point there could be a demand for Australian resources to supply the push to electrify everything. BTW I won’t tell you which, I’ll let you figure that out on your own.

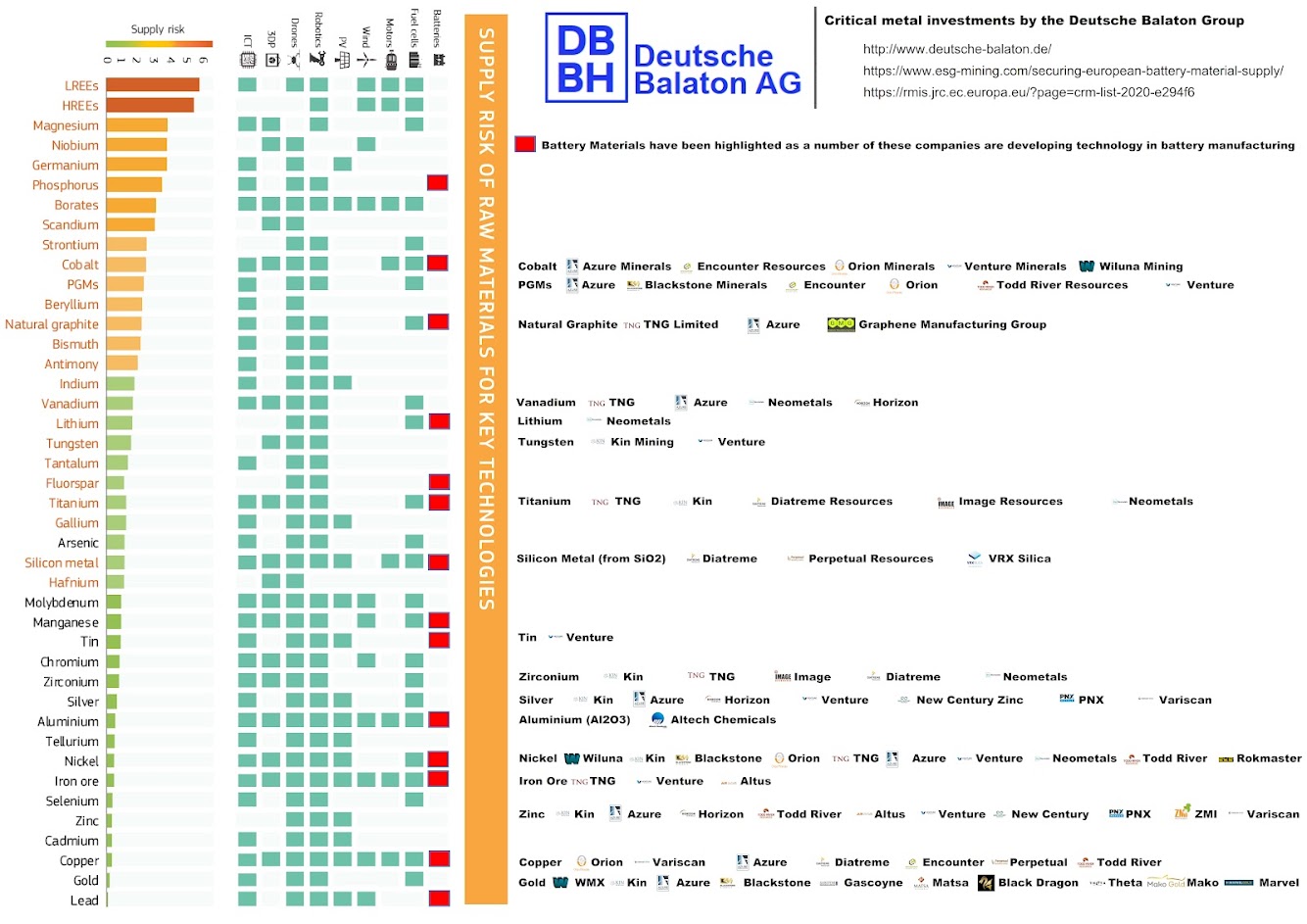

Needless to say, a quick look at Deutsche Balaton to see if they have anything of note to invest in seemed to be In order. So I started looking. The more I looked, the more I found. Their website has a list of companies but not many that look like resource companies. Certainly not all of the above.

So I decided to put together & classify their investments as per Softbank, Bezos, Koch Industries, Breakthrough Energy Ventures & Sumitomo. And this is what I ended up with.

So although their website isn’t really built to capitalize or advertise what the group have been assembling, once it is classified & posted it looks very similar to the industrial majors mentioned earlier.

But that then raises another question – the list of companies on the investment site were all mineral resource companies. So if Deutsche Balaton were investing in these companies, just how many were there, how much in terms of % of the company (were they looking to take them over), was it a passive or active investment & lastly what did the mining companies mine?

So circling back to the RIO Tinto Metals most impacted by new Technology chart put together by MIT & in order they were : Tin, Lithium, Cobalt, Silver, Nickel, Gold, Tungsten, Vanadium, Graphite, Niobium, Zinc, PGE or Platinum Group Metals (sometimes PGE / Elements) & Salt.

Well when all of the mineral exploration & production companies around the world which Deutsche Balaton have invested are classified, this is what it looks like.

Geographically

If all those European automobile manufacturers were looking ahead a few years from 2018 realising they will require significant amounts of materials which currently are not getting mined, you’d think they’d be trying to make sure that long term supply chains were in place. Electrifying everything is going to be not just a matter of trying to reduce pollution, but also of trying to drive down costs. The preceding pages have tried to spell out a number of different pathways to do just that for Lithium battery manufacturing. But it all comes to zero if everyone needs all the elements at the same time, because that will drive up raw material costs above consumer pricing points.

So what if someone recognized this long enough ago to plan for such a time?

Deutsche Balaton looks exactly like you’d expect an industrial major whose purpose was to secure the long term supply of critical minerals to ensure supply chains for European manufacturers are there long term, at a decent pricing point, in order to electrify everything.

These writings about the technical aspects of batteries, components, supply chain and the like are intended to stimulate awareness and discussion of these issues. Investors should view my work in this light and seek other competent technical advice on the subject issues before making investment decisions.